From 2013, while working at Cisco with large ICP operators (Internet Content/Cloud Providers), I observed the capex and opex themes, attributes, and value proposition for disaggregated network elements, standardized systems and subsystems — which are interoperable with other standard, multi-vendor solutions. Operators were looking to build their next generation cloud network architectures with not only best of breed products and technology, but also standard, merchant components and subsystems — driven by cost and time-to-capacity and operation agility — because their networks are large and they would consume many of the same network elements to standardize their architecture worldwide. They would qualify, deploy, and operate with few specialized resources and repeatable, automated processes.

I was informed by one such cloud operator that they would not be procuring the optical modules from the Network Equipment Manufacturers (NEM) used in it's systems. Instead, they would procure their selected optics directly from qualified module manufacturers. The objective was to eliminate OEM markup or margin stacking to reduce costs. The only exception was if the NEM system vendor would sell the OEM optics at the merchant market price (more on this later). That fact and market force echoed across all of the operators, and set a new trajectory for optical consumption models and architectures, and my career, for years to come.

In 2016, I accepted an opportunity to join Oclaro as Vice President of Business Development and Sales with a strategic focus on the ICP data center operator market worldwide. My objective was to develop new business opportunities with operators looking for direct consumption of optical modules, and to reduce the integration time, complexity, and transfer-ability of optical module solutions. Oclaro was the #1 supplier and market share leader of the pluggable Coherent optical transceiver module known as CFP2-ACO. CFP2 is a standard MSA module form factor. ACO is an acronym for 'Analog Coherent Optics’.

The architecture for ACO pluggable defines that the Coherent DSP reside outside of the module package on a host board or line card[1]. The analog circuitry and software integration for operation, control, and management of a CFP2-ACO requires specialized and customized integration by the system vendor. There is high dependency not only on the DSP integration, but also the Networking Operating System (NOS) of a particular platform. That integration effort took many months before a system could be released to the market, and the integration is not easily transferable to other system vendors and platforms.

Beginning in 2018, a standard host interface was being defined and implemented for optical transceiver modules to integrate with 3rd party NOS platforms. The standard interface is Transponder Abstraction Interface, or TAI[2]. TAI defines a vendor and form-factor independent method for controlling optical transponders and transceivers from different vendors.

https://telecominfraproject.com/oopt/

TAI is borrowed from, and common to, Switch Abstraction Interface or SAI[2], which is used by NOS vendors to integrate the control, management, and data plane of merchant switch ASICs (such as Broadcom Tomahawk or Innovium Teralynx) in ODM whitebox switch platforms. TAI is hosted by Telecom Infra Project (TIP)[3] Open Optical and Packet Transport (OOPT) working group[4], led by Facebook.

Also on the horizon at the time was Digital Coherent Optics (DCO) modules[5]. A DCO transceiver integrates the DSP inside the optical module, with standard defined digital communications interface to the host board.

https://www.accton.com/Technology-Brief/coherent-optics-efficiency-capacity/

DCO significantly reduces the system and software integration time, and greatly improves time to market and operator service velocity from months to weeks. Our next gen CFP2 Coherent transceiver module, a DCO, was many months away from production. But in 2018, I had ACO production modules, DCO beta samples, and TAI. All I needed was a system and NOS platform to integrate, test, and take to market.

Edgecore, a whitebox vendor and subsidiary of ODM manufacturer Accton, was developing an integrated packet optical switch. It entered the market with its Cassini platform[6].

https://www.edge-core.com/productsInfo.php?cls=1&cls2=345&cls3=346&id=605

Cassini was a 2nd generation whitebox packet optical switch to the 1st generation Voyager platform introduced by TIP in November 2016[7]. Cassini is based on the OCP Wedge Switch architecture (32 ports x 100G I/O), but with 8 line cards to host CFP2 modules which could be either or both ACO and DCO. I partnered with IP Infusion, an ISV NOS developer for the whitebox switching and routing market[8], to integrate the ACO and DCO Coherent Optics modules in the Cassini switch platform. Armed with confidence and a small internal team and ecosystem partners, we set out to demonstrate a multi-vendor, open, pluggable, interoperable, and flexible packet optical switch solution. Our target date and event was TIP Summit - London, October 2018.

Open Packet Optical Interoperability Demo, TIP Summit - London, October 2018

Our team succeeded in attaining the goal we set out to accomplish, as noted: TIP Community Achieving Significant Momentum on the Path to Open, Interoperable, Disaggregated and Standards-based Networks[9]. The first mission objective was accomplished. With that successful achievement we had a marketable product with ecosystem partners. Each partner sought mutual success in a new market opportunity. Each had its own customers, sales organizations, and channels to market. We had the foundation of a "Networking Effect”. Our confidence was very high with Go-To-Market strategy and product roadmap for DCO optics.

At the same time, the

traditional Network Equipment Manufacturers (NEMs) had taken notice of

the massive shift in system BOM cost and value to the optical I/O

modules, as well as the innovations and standards efforts leading to open, pluggable, and interoperable modules. Ciena was vertically integrating the development of its

optical solutions with the acquisition of Teraxion[10]. Cisco made a bid

to acquire Acacia[11], a vendor of Coherent DSPs, integrated Silicon

Photonic components, and a merchant module vendor.

In December

2018, Lumentum acquired Oclaro[12]. I accepted the transfer and organizational role

change from Oclaro to Lumentum. The

assignment: Global Business Development reporting to the SVP/GM (also from Oclaro). The Mission: take the ACO and DCO

optical modules to market, and continue developing and participating in the

open networking market ecosystem. The role had underlying risks. Most notable was the internal tug-of-war conflict between NEM customers and

the merchant supply of competing solutions, such as Lumentum branded

commercial modules[13].

In 2019, in collaboration with Telecom Infra Project (TIP) and Open Networking Foundation (ONF)[14], we began to develop and interleave with partners to create an ecosystem — from ODM whitebox and ISV vendors, to VAR/SI channel partners. We held joint customer meetings, conference and trade show appearances, presentations, webinars, and sharing of content, messaging and positioning material. That effort resulted in operator trials — from the lab to the field. Here we succeeded again: Cassini Packet Transponder field trial demonstrates multi-format transmission with multi-vendor, open packet optical network elements, at Telefónica del Perú[15].

https://whitestack.com/20191111-whitestack-cassini-trial-at-telefonica-peru/

At the same time in 2019, the OIF 400ZR standard specification[16] and OpenROADM MSA[17] solutions were on the horizon. With deep conviction that 400G DCO modules would encourage open optical network architectures and consumption models, in particular the QSFPDD-400ZR would be the inflection point in the market for convergence of packet/optical (IP/DWDM) and would transform the market and operator networks, I led Lumentum to participate in the OpenZR+ MSA[18].

In May 2019, I presented at NGN DCI Summit in Nice, France — The role of DCO in overcoming bandwidth and reach limitations[19], and participated on several conference panels. The thesis and research I projected was a convergence and inflection point of broad market adoption of DCO at 400G. The drivers: packet/optical I/O convergence and the standardization of module form factor, electrical host communications, and optical line side forward error correction (FEC). The capex and opex benefits were obvious to me. My research found operator surveys projecting the 5-year adoption rate to reach 50% and $1B TAM by 2023. I maintained that 200G DCO was a stepping stone path into the market: to develop sales, partners, and channels while R&D/PLM simultaneously develop 400G DCO modules for the QSFPDD-400ZR/ZR+ applications, and CFP2-400G DCO for OpenROADM applications[20].

The role of DCO in overcoming bandwidth and reach limitations[19]

The successful field trial at Telefonica del

Peru[21], a challenging metro and diverse path long haul fiber network

consisting of both old and degraded fiber to aerial fiber routed over

mountain terrain, gained much notice at OFC 2020 — as presented by

Geraldine Francia of Telefonica: Disaggregated Packet Transponder field

demonstration exercising multi-format transmission with multi-vendor,

open packet optical network elements[22].

The success with Telefonica, and WhiteStack as the lead integrator in South America, subsequently led to a first operator deployment with Mundo Pacifico in Chile: Mundo Pacífico activates HyperNET, the first disaggregated optical network in Latin America, using Cassini from Telecom Infra Project[23]; Mundo Pacifico selects IP Infusion and Whitestack for deploying the first disaggregated optical network in Latin America[24]. Our success in South America led us into the Brazil market with CPqD, a TIP Community Lab partner, in a PoC trial for regional service providers.[25] The momentum continued in 2020 with the first deployment of an open packet optical solution in Burkina Faso, Africa: VTS Launches First Commercial Deployment of TIP’s Cassini Solution in Africa[26].

400G

DCO modules will be commercially available in 2021. The HW/SW ecosystem vendors are ready. The NEM

vendors have taken notice. Large operators including AT&T[27], Comcast[28], Microsoft[29], Telia[30], Verizon[31], and Windstream[32] have all publicly showcased trials and operational deployments

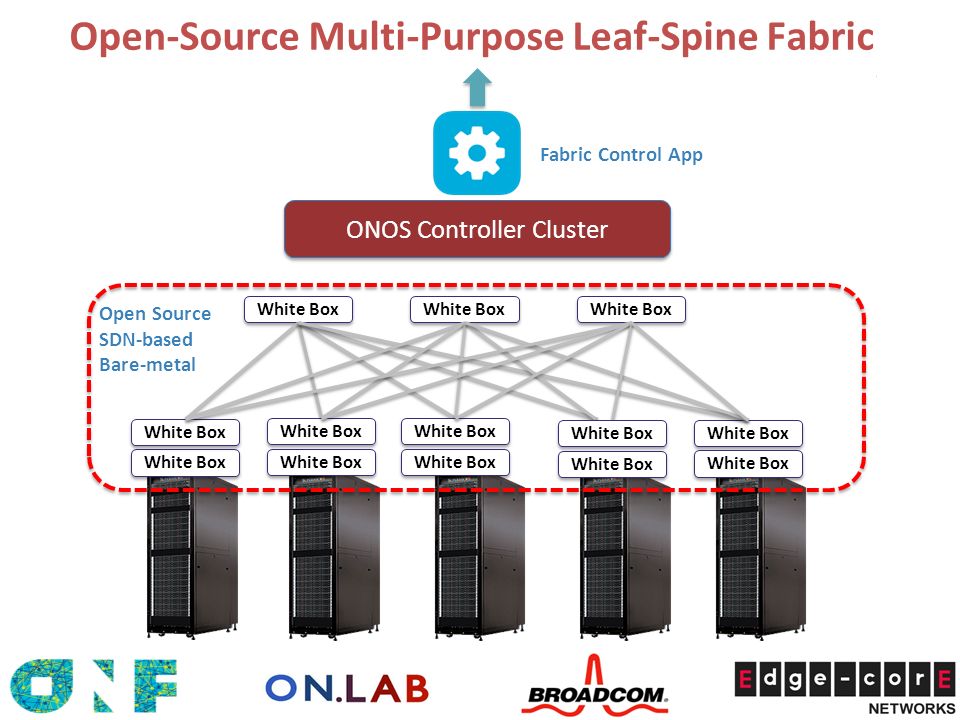

of dissagregated elements — from UfiSpace ODM Whitebox hardware running Cisco

IOS, and ONF Trellis distributed CLOS access network architecture using Whitebox switches, to 400ZR/OpenZR+ application and interoperability results.

https://techblog.comsoc.org/2019/09/14/comcast-puts-onf-trellis-software-into-production/

The industry trend is toward networking elements that are: Open, Standard, Pluggable, Interoperable, and Disaggregated, with direct sourcing and supply arbitrage strategies. Capable component and module vendors are pivoting into this open market. Some suppliers are choosing to remain a captive supplier rather than be a merchant supplier of open optical modules. NEMs have moved to vertically integrate to capture more value (share of operator wallet spend), by developing or acquiring optical components (IP), and subsystems module vendors. The operator market spend is open to all vendors for share capture.

NEMs

with merchant optics lines are expected to yield good attach rates with their

platforms, but could also sell their optics as disaggregated merchant solutions to capture value in a competing vendor's switch or router platform. After all,

the system BOM cost with 100G to 400G optical I/O ports is 50-70%,

respectively, thus marginalizing or commoditizing the system hardware and software. Each share of wallet spend captured from the competitor, in any market, is market share gain and a value position attained.

We are on the heels of a waning global pandemic and on the cusp of one of the largest network transformations in history. From edge networks to core networks, the open ecosystem will generate billions of dollars in new value. Those vendors that do not pivot will miss a significant market opportunity. The market is moving. The journey toward open, standard, pluggable, interoperable optical networks will be realized in 2021.

References:

[1] https://en.wikipedia.org/wiki/Coherent_optical_module#Analog_Coherent_Optics_(ACO)

[2] https://github.com/Telecominfraproject/oopt-tai

[3] https://telecominfraproject.com

[4] https://telecominfraproject.com/oopt

[5] https://en.wikipedia.org/wiki/Coherent_optical_module#Digital_Coherent_Optics_(DCO)

[6] https://www.edge-core.com/news-inquiry.php?cls=1&id=258

[7] https://www.facebook.com/Engineering/posts/at-the-first-telecom-infra-project-tip-summit-today-facebook-announced-voyager-a/10154588449747200/

[8] https://www.ipinfusion.com/products/ocnos/

[9] https://telecominfraproject.com/tip-community-achieving-significant-momentum-on-the-path-to-open-interoperable-disaggregated-and-standards-based-networks/

[10] https://www.ciena.com/about/newsroom/press-releases/Ciena-Acquires-TeraXion-Assets_prx.html

[11] https://newsroom.cisco.com/press-release-content?type=webcontent&articleId=2000889

[12] https://www.lumentum.com/en/media-room/news-releases/lumentum-announces-completion-oclaro-acquisition

[13] https://www.lumentum.com/en/products/cfp2-dco-100g-200g-pluggable-transceiver

[14] https://opennetworking.org/reference-designs/odtn/

[15] https://www.whitestack.com/posts/20191111-whitestack-cassini-trial-at-telefonica-peru/

[16] https://www.oiforum.com/technical-work/hot-topics/400zr-2/

[17] http://openroadm.org/

[18] https://openzrplus.org/

[19] http://investor.lumentum.com/investors/financial-news-releases/financial-release/2019/Lumentum-To-Exhibit-At-Four-Tradeshows-In-The-Next-Three-Months/default.aspx

[20] https://event.on24.com/eventRegistration/EventLobbyServlet?target=reg20.jsp&partnerref=Fujitsu&eventid=2106754&sessionid=1&key=AEBDEC0D296AFB06DE3615F774B65E06®Tag=&sourcepage=register

[21] https://www.semanticscholar.org/paper/Disaggregated-Packet-Transponder-Field-Exercising-Francia-Nagase/96236ea323db903f8a2c534c82eaab54dc635311

[22] https://www.osapublishing.org/abstract.cfm?URI=OFC-2020-Th3A.1

[23] https://www.whitestack.com/posts/20200720-hypernet/

[24] https://www.businesswire.com/news/home/20200721005166/en/Mundo-Pac%C3%ADfico-selects-IP-Infusion-and-Whitestack-for-deploying-HyperNET-the-first-disaggregated-optical-network-in-Latin-America

[25] https://telecominfraproject.com/transport-trial-test-report, and https://www.lightwaveonline.com/network-design/packet-transport/article/14198848/cpqd-reports-on-tip-cassini-dcsg-transport-trials-in-brazil

[26] https://telecominfraproject.com/vts-launches-first-commercial-deployment-of-tips-cassini-solution-in-africa/

[27] https://about.att.com/story/2020/cisco_att.html

[28] https://techblog.comsoc.org/2019/09/14/comcast-puts-onf-trellis-software-into-production/

[29] https://www.lightwaveonline.com/optical-tech/transmission/article/14197886/arista-confirms-400g-zr-optical-transceiver-interoperability-with-microsoft

[30] https://www.teliacarrier.com/about-us/press-releases/tc-pluggables-using-acacias-modules-cisco.html

[31] https://www.lightwaveonline.com/data-center/data-center-interconnectivity/article/14184103/verizon-media-uses-inphi-colorz-ii-for-400zr-trial

[32] https://www.lightwaveonline.com/optical-tech/transmission/article/14198175/windstream-wholesale-runs-400g-zr-transmission-more-than-1000-km-in-live-network

No comments:

Post a Comment